The Australian Prudential Regulation Authority (APRA) recently proposed increasing the total capital requirements of authorised deposit-taking institutions (ADIs) (particularly the four majors) in order to further strengthen the financial system. APRA wants to lift total capital requirements for the four major Australian banks by 4-5% of risk weighted assets (which equates to around a further $75 billion of additional capital) within five years. under the proposals the Major Banks will be required to have a total capital buffer of around 19%, up from 14.5%. Since 2015, APRA has already ordered the big four banks to boost capital levels twice.

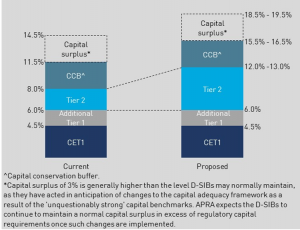

The regulator stated any form of capital can be used but it expects the bulk of the funds to be raised via Tier 2 capital to meet the proposed higher capital requirements as seen below. On the capital structure, Tier 2 capital ranks above common equity and Tier 1 hybrids, and below senior unsecured bonds so this would provide additional buffer to holders of senior unsecured bonds.

Proposed change to the Major Banks’ capital structures – as a percentage of RWA

Source: APRA

Credit ratings agencies view APRA’s proposal as credit positive for the banking industry though the stricter standards are unlikely to result in higher credit ratings for the banks. S&P though stated if APRA’s proposal turns into regulation, S&P may upgrade its outlook for the major banks’ senior bonds from ‘negative’ to ‘stable’. Moody’s and Fitch both currently have stable outlooks on the ratings for the major banks, hence no change on the ratings outlook is expected.

S&P also added that APRA’s proposed new capital requirements “could lessen the need for the Australian government to recapitalise these banks if they were to experience distress”. However S&P also added “In our view, the proposal suggests no impediments or change in [the] Australian government’s attitude to bailing out a systemically important bank, if needed.”

This last point is important to appreciate as on a stand-alone basis the major banks have an “A-” credit rating which is only upgraded to “AA-” due to implied government support; hence the major banks’ overall credit ratings are very much influenced by judgements as to whether the Australian government’s support for the banks is getting stronger, weaker or remaining the same. The capital raising should increase the underlying credit-worthiness of the banks on a stand-alone basis, but if it does not alter the government’s willingness and ability to support the banks in a crisis, it is unlikely to result in a ratings upgrade.