Amicus regularly receives enquiries from clients regarding appropriate benchmarks for their portfolio against which they can measure investment performance. There is no singularly correct answer as to the “best” benchmark to use but some benchmarks are clearly more appropriate than others. In general, a “good” benchmark is one that represents a practical alternative carrying a similar risk profile where investments could be made.

For example, a good benchmark for an equity fund manager investing in large Australian companies might be the ASX 200 as potential investors in the fund would likely be looking to gain exposure to leading Australian equities and perhaps would wish to invest in the actively managed fund if its performance was better than the index (after fees). Investing in the index through an index tracking fund is an alternative investment and a comparison would show the value added (or not) through the active manager’s strategies. Conversely, the ASX 200 would not be a good benchmark for a conservative cash fund as potential investors in the cash fund would presumably be looking for an entirely different risk profile to that presented by equities and the cash fund performance is not comparable to that of the index as they are exposed to entirely different investment instruments.

An alternative approach is not to look for performance relative to an index but to look at absolute returns or those relative to inflation. The logic with looking at “real” or inflation adjusted returns is many investors are looking to maintain or increase the purchasing power of their capital and income, i.e. after adjusting for the effects of inflation. This type of benchmark is generally more appropriate for those looking at absolute returns rather than relative performance to a specific asset class to assess the skill of the investment manager.

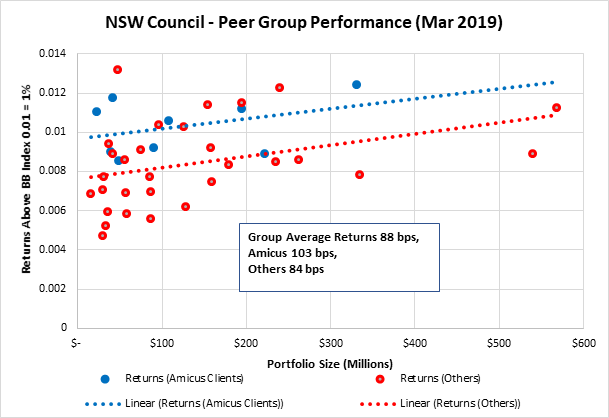

Another approach to benchmarking is to measure performance against industry peers which strips out the effect of market conditions. For conservative investors, this is an important consideration as opportunities to enhance returns vary greatly with market conditions, primarily the level of credit margins and the absolute level of interest rates. This is one of the reasons Amicus provides six-monthly peer review to clients. We attach below a graph of returns for the peer group of NSW Councils (as of March 2019 as measured relative to the Bloomberg Bank Bill Index – a common and appropriate benchmark for conservative investors such as NSW councils).

The blue markers on the graph represent the performance of Amicus advised clients and the red markers represent the performance of Others (those councils without an advisor, or advised by brokers, platform providers or other independent advisors). While there is dispersion within the results, the red and blue dotted lines represent the best fit straight lines through the respective coloured markers. The red and blue lines both slope upwards reflecting the trend to better performance with large portfolios. The blue line is on average around 20bps above the red line showing the value of independent advice (from Amicus) over a combination of advice from other advisors, no advice, or advice from brokers and platform providers who tend to recommend the products they are selling with a conflict of interest towards the ones that offer them the largest margins or commissions.

Ultimately, we recommend clients look at a range of benchmarks to assess their performance against different metrics depending on their specific circumstances. The above is an abridged version of a detailed article provided to Amicus’ clients. Please contact us if you want to get further details or if you need assistance in choosing appropriate benchmarks for your portfolio.